The OS for the

UGC Apps Economy.

Create. Distribute. Manage. Monetize. The most efficient way.

We give every creator the infrastructure that used to belong to studios.

What the hero says, decompressed: apps are now user-generated content. Anyone can ship one in a weekend with Lovable, Cursor, Bolt, Claude Code. Creation is no longer the bottleneck.

The bottleneck moved to everything after the prompt, distribution to real users, retention, attribution, identity, support, monetization. Each piece used to belong to well-funded studios. They had AppsFlyer, Vercel, Mixpanel, Customer.io stitched together with engineering budget.

@appssPro is that whole stack, but native to the substrate where the audience already lives: messengers becoming superapps. Telegram first. LINE, Discord, TikTok-mini next.

And critically, we don't have to charge $19/mo for the toolkit. The audience their apps bring into our store is what we monetize. Aggregator economics, not classical SaaS.

Apps are now user-generated content.

Monthly app releases doubled since Jul 2025. The AI-builder wave hit.

Apple App Store

Apple App Store Lovable ARR

Lovable ARR Claude Code

$2.5B ARR · WAU ×2

Claude Code

$2.5B ARR · WAU ×2

Cursor

7M devs · $2B ARR

Cursor

7M devs · $2B ARR

Copilot

20M devs · 4.7M paid

Copilot

20M devs · 4.7M paid

OpenAI

$12B ARR · 800M weekly

Lovable

OpenAI

$12B ARR · 800M weekly

Lovable Bolt

Bolt v0

v0 Replit

Replit FlutterFlow

FlutterFlow Gemini

GeminiA year ago, shipping a native iOS app meant a team and a deadline. Today Cursor and Claude Code write the Swift directly inside Xcode, Apple itself shipped the Claude Agent SDK as part of Xcode 27 at WWDC last week. Copilot and Codex do the same in Android Studio. Replit Agent and FlutterFlow ship straight to the App Store from a prompt. The result: 235K new iOS apps in Q1 2026, +84% YoY, the biggest quarterly jump in a decade. 2025 closed at 557K new apps, Apple's first +24% year since 2016.

And it's not studios anymore. Anthropic says 80% of its own production code is now written by Claude. Cursor crossed 7M developers and $2B ARR. JetBrains' 2026 developer survey found Claude Code adoption at 75% inside small startups. Apps that used to take a quarter and a team now take a weekend and a prompt. The supply of apps just doubled, and the people supplying them are the same people who post Reels.

But Andreessen Horowitz published the most-quoted essay of the year on this, Most People Can't Vibe Code. The argument: vibe-coding so far has reached only the technical 1%, developers, founders, designers, PMs. Everyone else still watches AI demos as spectator entertainment, not something they could attempt themselves. Justine Moore frames the real opportunity as the ~65M non-technical creators who could ship apps if four problems get solved: zero-friction setup (no SSH, no envs), built-in security (≈50% of AI-generated code today ships with vulnerabilities), imagination (templates, discovery, social feeds, non-technical users can't envision what's possible alone), and one-click deployment (the «localhost» problem). a16z's framing: «tools give you capabilities to build something yourself; products give you the outcome you're looking for.» Whoever ships the product, not the tool, becomes Squarespace for the next generation of software.

Apps now live like Reels.

Created → hooks attention → converts → decays → next. Same lifecycle as content. Just with stronger conversion.

Reel · TikTok · Short

Reel · TikTok · Short

- 1Created, record 30s in the same app you'll post in

- 2Posted, algorithm tests reach in seconds

- 3Hook, first 3 sec capture attention, or scroll

- 4Convert, fun · share · follow · link tap

- 5Decay, algorithm moves on, attention spent

- 1Vibe-coded, built in days, inside the network you'll post in

- 2Deployed, 1 tap inside TG · IG · TikTok · WA

- 3Hook, «answer 5 questions, see your match»

- 4Convert, buy · share result · refer a friend

- 5Decay, trend cools, app archived

The classic app lifecycle ran in years. Build for 12–24 months, optimize retention, fight for every percent in DAU, hope to survive a decade. The unit-economics required well-funded studios and venture timelines.

The UGC-app lifecycle runs in weeks. A creator vibe-codes an idea in days, deploys natively across messengers in one tap, posts content about it in the same network, and lives off the peak. When the trend cools, the app archives. The strongest mechanic gets ported into the next one.

The unit-economics flip

Classic app: $50K–$5M cost · 6-24 months build · 3-10 year lifecycle if it survives · few big bets · binary failure cost.

UGC app: $0–$5K cost · days-weeks build · 2-12 week active phase · many small bets · negligible failure cost.

The same mechanic gets iterated, improve hook, port the format to a new niche, ship the next observation as its own app. Compound advantage moves from any single app → creator's reputation and audience, exactly how it works for YouTubers and short-form creators today.

The top apps are becoming app stores.

9 of the top 10 already host an app surface. 3 run full mini-app stores · the rest run chatbots, games, or interactive posts.

| # | App | MAU | App surface |

|---|---|---|---|

| 1 |  Facebook Facebook | 3.07B | ✓Instant Games |

| 2 |  WhatsApp WhatsApp | 3.0B | ✓Flows (Chatbots with basic UI) |

| 3 | Instagram | 3.0B | ✓DM Chatbots |

| 4 | YouTube | 2.7B | ✓Playables (Games) |

| 5 | TikTok | 1.6B | ✓Minis |

| 6 |  WeChat WeChat | 1.41B | ✓Mini Programs |

| 7 |  Telegram Telegram | 1.0B+ | ✓Mini Apps |

| 8 |  Reddit Reddit | 765M | ✓Apps, Interactive Posts |

| 9 |  Messenger Messenger | ~700M | ✓DM Chatbots |

| 10 |  X X | 586M | , |

| App | Top # | Region | Last significant update |

|---|---|---|---|

| WhatsApp | 2 | 🌐 | Sep 2025 · Flows v7.2 + Image Carousel |

| WeChat | 6 | 🇨🇳 | Jan 2026 · 70 mini-games > 1M DAU |

| TikTok | 5 | 🌐 10 reg. | Dec 2025 · Minis live in 10 markets |

| Facebook + Messenger | 1 · 9 | 🌐 | Aug 2025 · Instant Games SDK v8.0 |

| Telegram | 7 | 🌐 | Mar 2025 · 1B MAU + Stars monetization |

Alipay Alipay | , | 🇨🇳 | Nov 2025 · Apple cuts mini-app fee to 15% |

LINE LINE | , | 🇯🇵 Asia | Oct 2025 · Web access + ads + IAP |

Discord Discord | , | 🌐 Gaming | Mar 2026 · Game Shop + Social Commerce |

KakaoTalk KakaoTalk | , | 🇰🇷 | Sep 2025 · Feed redesign + Kanana AI |

Zalo Zalo | , | 🇻🇳 | Dec 2025 · 1,205 government mini-apps |

Snapchat Snapchat | , | 🌐 | , · Discontinued 2022 (dormant) |

The world's top apps no longer compete on features, they compete on how much of the user's day they absorb. The end state of that competition is the super-app: every adjacent need (shopping, payments, games, productivity) gets a mini-app surface inside.

WeChat showed the pattern (2017). 4.3 million mini-programs, more apps than Apple App Store and Google Play combined. Average user runs 9.8 of them per day. 945M MAU live inside the surface, not the OS.

Telegram followed (2023), TikTok joined (2025), Apple acknowledged in Nov 2025. Every billion-user messenger or super-app on Earth has either opened a mini-app surface, or is in the process of opening one.

What «app surface» means per platform

- Full mini-app stores: WeChat Mini Programs, Telegram Mini Apps, TikTok Minis, third-party app catalogs with discovery, payments, runtime.

- In-conversation apps: WhatsApp Flows (multi-screen UI inside chat), Instagram + Messenger DM chatbots (Send/Chat APIs).

- Embedded games / interactive surfaces: Facebook + Messenger Instant Games (HTML5), YouTube Playables (browser games inside YT), Reddit Devvit + interactive posts.

- Not yet: X, payments licensed (X Money / Visa), no third-party app surface shipped despite the «everything app» pitch.

By region

- East Asia: WeChat (1.41B), Alipay (720M+), LINE (97M JP), KakaoTalk (50M KR), Zalo (79.6M VN), most mature, most penetrative

- Global / cross-border: Telegram (1B+), TikTok Minis (10 regions), Discord Activities (200M)

- Western / Meta family: Facebook + Messenger Instant Games, Snap Mini, WhatsApp Flows

Apple Mini Apps Partner Program · Nov 13, 2025

Apple halved its commission to 15% for qualifying mini-apps hosted inside a parent native app. Tencent / WeChat signed up first. This is Apple, the strongest gatekeeper in mobile, formally embracing the super-app model that started in Asia and now ships globally.

«One pattern. Eleven hosts. The mini-app surface won.»

Vibe-coding Verticals Matrix.

@appssPro takes the full suite for the mini-apps vertical, and approaches the native stack.

- @appss Market Research · AppMagic · Sensor Tower

- @appss Builder + Designer · Lovable · FlutterFlow · Figma

- @appss Mini-app Remix only @appss

- @appss Hosting · Vercel · Firebase

- @appss Analytics · Mixpanel · Amplitude

- @appss Push + CRM · OneSignal · HubSpot

- @appss Attribution · AppsFlyer · Adjust · Branch

- @appss Subscription Mgmt · Stripe · RevenueCat

- @appss Influencer Marketplace · Modash · HypeAuditor

- @appss APIs · OpenRouter · RapidAPI · Apify · Phantombuster

- @appss Store · Apple App Store · Google Play

Base AI tools cover everything, slowly. Builders cover web and native. Infra + launch tools cover web and native. Below the build layer, mini-apps are abandoned. That's the blue ocean. @appssPro is the full stack, built for it.

Row ①, Base AI coding works everywhere (Claude Code can write iOS code, web React, or a Telegram bot). But it's slow, manual, and the creator carries every decision. Few non-devs use it productively.

Row ②, Builders compress weeks to hours by bundling decisions + infra. Web and native have a dozen mass-market players each. Messenger mini-apps have almost no turn-key builders, what exists is either platform-owned dev kits (WeChat Devtools, LIFF, TikTok H5) or niche tools that target one ecosystem and one use case (SODA = TG memecoin games; ManyChat = WA flows).

Row ③, Infrastructure for messengers is structurally different. Each super-app gatekeeps its own runtime. You don't pick «hosting»; you deploy to Tencent / Meta / TikTok endpoints, or self-host the webview on Vercel. No third-party «messenger-native infra-as-a-service» exists.

Row ④, Launch tools. This is the deepest gap. Web has Mixpanel + Stripe + OneSignal + Customer.io. Native has AppsFlyer + Adjust + RevenueCat. For messenger mini-apps: Mixpanel works if you wire it manually; nothing else has been built. No AppsFlyer equivalent, no push-orchestration, no native subscription management, no creator-attribution layer. That's where @appssPro plays.

Why this matters

The further down the stack you go, the more domain-specific tooling becomes. The further down the messenger column you go, the emptier it gets. The gap isn't a feature, it's an entire category.

«Build is commodity. We sell what comes after, natively, for the surface no one else serves.»

There's  .

.

And there's  .

.

One stack. Two surfaces. Creator OS on one side. Discovery store on the other.

@appssPro, the OS for shipping & growing.

The full launch cycle in one workflow. Research → build → distribute → monetize. Native to the mini-app surface where the creator's audience lives.

- 12 capabilities under 4 phases

- One subscription replaces 10 services

- AI-action surface: Claude / ChatGPT drive it

- Per-app + per-team pricing

@appss, the discovery store with a social graph.

Where users find, install, review, follow, and earn. Bridges native + mini-app worlds. Each install travels with the user's social context built-in.

- App profiles · reviews · followers

- SEO + AIO (GPT/Claude discovery)

- Earn, staking, bounties, partner programs

- Cross-surface bridge: native ↔ messenger

@appssPro is what creators pay for (and ship from). It's a launch-cycle OS: market research, build, design, host, distribute, attribute, push, monetize, support, natively for the mini-app surface they choose.

@appss is the consumer-facing store, installed inside Telegram today, ported to messengers next. Users browse, review, follow creators, stake Stars, earn. It's a YouTube-shape consumer surface, not a curated catalog.

Why two products on one stack

Every app shipped through @appssPro lands in @appss. Every user on @appss becomes a candidate for installing more apps. Both products compound each other. Vercel + AppsFlyer + Lovable could never have done this, they had no audience aggregator on top.

«One subscription replaces 10 tools. One store distributes them all. The economics are SaaS at the floor and aggregator at the ceiling.»

covers the

full launch cycle.

Thirteen capabilities. Four phases. One creator workflow, natively for messenger mini-apps.

- Market Research AI

- Mini-app Remix

- Designer Studio

- Builder

- Hosting

- APIs

- App Store Listing

- Influencer Market

- Social Tracker

- Referral Program Management

- URM (user mgmt)

- Push Management

- Support Module

Each capability replaces a stand-alone tool from the web/native world, but built around messenger primitives (Stars, init_data, channel attribution, bot rails) so it actually works for mini-apps.

Why bundled vs. picked à-la-carte

Mini-app creators don't have engineering budgets to glue 10 stand-alone tools. They need one cohesive workflow where build → ship → grow → monetize happens in continuous flow. We sell the workflow, not the parts.

AI Plays on top

Each capability exposes an AI action surface, Claude / ChatGPT plug in and drive any of the 12 capabilities through chat. «Track this competitor app», «Send a push to my churned cohort», «Generate a referral landing», all happen inside the chat thread, executed against the stable stack.

«Build is commodity. We sell the full launch cycle as a single creator workflow.»

Know the market before you build.

Two products that turn «I have an idea» into «I have proof someone wants this».

Market Research AI

Market Research AI Mini-app Remix only @appss

Mini-app Remix only @appssMost app failures aren't engineering failures. They're market-signal failures: building a feature nobody wants, ignoring a category that's exploding, missing the monetization signal in a competitor's launch.

Market Research AI

The agent sees our entire indexed catalog, 8K+ apps with parsed events, MAU/retention data, push patterns, Stars distribution, partner-program flows. Founders ask natural-language questions; the AI answers with charts, comparable apps, and concrete benchmarks.

Mini-app Remix · the unique one

The Builder API can read any catalog app's structure: screen-by-screen layout, event funnel, monetization hooks, push schedule, referral mechanic. Remix turns that read into a starter project. The founder modifies brand, tweaks copy, swaps monetization, and ships a substantially different app that starts from proven mechanics, not blank page.

«Most apps start from a wireframe. @appssPro-built apps start from a working competitor schema.»

Ship a working app in an afternoon.

Four products that compress the «design → build → host → integrate» cycle from weeks to hours.

Designer Studio

Designer Studio Builder

Builderinit_data, Stars, channels, bot rails natively. Output = production-ready mini-app + versioning + one-click deploy. Hosting

Hosting APIs

APIsEvery Build capability is shaped by one observation: the messenger substrate has its own primitives (auth via init_data, payments via Stars + Tribute, distribution via channels). Generic web/native builders don't speak any of it.

Designer Studio

The brand-agent learns once (logo, palette, voice, mood), then generates everything: app covers, in-app screens, promo posters, push thumbnails, app-store listing assets, all consistent. Founders stop hand-managing brand artifacts.

Builder + Hosting

Substrate-aware code generation. The Builder knows that init_data must be verified server-side, that Stars need invoice setup, that channel-driven distribution requires bot integration. Hosting is the production-ready endpoint where everything ships.

APIs · the resold layer

Two products in one: (1) LLM keys at markup, saves creators from juggling 5 provider accounts. (2) Real-time parsing, Instagram / Telegram / TikTok trends, marketplace prices, search results. Lets founders build agentic apps that pull live data, not stale snapshots.

«The Build layer isn't just an editor. It's a substrate-aware compiler from idea → production mini-app.»

Find the first 10,000 users.

Four products that route audience from where it lives, channels, influencers, neighbors, into your app.

App Store Listing

App Store Listing Influencer Market

Influencer Market Social Tracker

Social Tracker Referral Program Management

Referral Program ManagementNative app stores reward ranking, paid placement, and category browse. Mini-app surfaces reward social signal, a friend shared, an influencer voted, a referral paid out, a creator-channel reposted. Distribution tools must match that shape.

App Store Listing

Founders get a hosted page in @appss store with optimized SEO + AIO out of the box. Indexes properly with Google + Claude/GPT discovery. Translates regionally without manual work.

Influencer Market + Social Tracker

Two-product play. Market = where you find + book influencers (490K indexed). Tracker = where you measure them after they post. Together = the closed loop AppsFlyer doesn't offer for messengers.

Referral Program Management

Configures the substrate-native referral mechanic that Telegram uniquely allows: multi-tier, chained, paid in Stars. Auto-tracked through init_data, no fragile cookie / fingerprint tricks needed.

«AppsFlyer measures iOS. We measure messenger graphs. Different game.»

Keep them, earn from them.

Three products that turn one-time installs into lifecycle revenue.

URM (User Relationship Mgmt)

URM (User Relationship Mgmt) Push Management

Push Management Support Module

Support ModuleMonetize isn't a single moment of payment. It's the ongoing relationship that turns a one-time visitor into a $50-LTV user, a referrer, an audience member who installs the next app on the stack.

URM · the spine

Every user state flows here: install source, payment status, push engagement, referral activity, last-active timestamp, predicted LTV. All cohortable, all queryable by Claude through MCP (see slide 13).

Push Management

1.04M deliveries already audited. Cohorted, behavior-triggered, brand-aware (Designer context). The push isn't «blast everyone», it's «churn-recovery to 4,127 users who haven't opened in 7 days, in their language, in your brand voice».

Support Module

Cuts support load 60–80% by clustering tickets (AI groups by intent), drafting replies (AI generates with knowledge base context), and surfacing patterns (founder sees «12 users hit the same bug today»).

«Stripe shows you payments. @appssPro shows you the user who paid, who churned, who came back, and what to send them next.»

, the persistence layer

for the AI client of your choice.

MCP-connected in 3 steps. Run the full stack from Claude · ChatGPT · Cursor, whichever you already use. The intelligence is theirs. The state is ours.

Claude

Copilot

Antigravity

Gemini

Cursor

Codex

Antigravity

Gemini

Cursor

Codex

via MCP

https://appss.pro/api/mcp

3Sign in · run

Investors ask: «if creators can just talk to Claude, why do they need @appssPro?»

The split

AI is brilliant at generation: writing copy in a brand voice, drafting a marketing campaign, hypothesizing why retention is weak, picking creative directions. It's useless at persistence: it doesn't remember which users got which push, which cohort opened, who paid, what the brand asset library looks like, how the catalog evolved last week.

@appssPro is the opposite: brilliant at persistence (production-grade DB, audited push delivery, cohort history, payment ledger, brand library), and intentionally not in the creative-generation business. AI does that part.

MCP, the bridge

Three-step plug-in (same shape vibiz.ai uses). After that, Claude can read any of our 13 capabilities, and execute through them. Creator never leaves their chat, but everything happens against persistent state.

The moat

This means we are the thing every AI operates through in the messenger-mini-app world. As AI models compete and get cheaper, the value migrates to whoever owns the action surface + state. That's us.

«AI brings the intelligence in the moment. We bring the state across all moments.»

@appss, App Store with a social graph.

@apps store on Telegram. Users browse the catalog, vote for what's worth shipping, earn for driving installs, and follow the creators behind each app.

Native app stores are algorithm-driven: top-50 takes everything, long-tail dies, no social signal. Mini-app surfaces have no catalog at all. @appss is built for the new shape: social-graph + community + earn.

① App Store basics, the floor

Catalog browse, app detail pages, ratings, reviews, screenshots, version history. 8.3K apps live. 49K reviews from 35K reviewers. The fundamentals creators expect.

② Product Hunt mechanics, community gating

Weekly «highest voted» surfaces. 🔥 vote leaderboards. Founders mobilize their community to vote; users discover what actually delivers value (not what bought ranking).

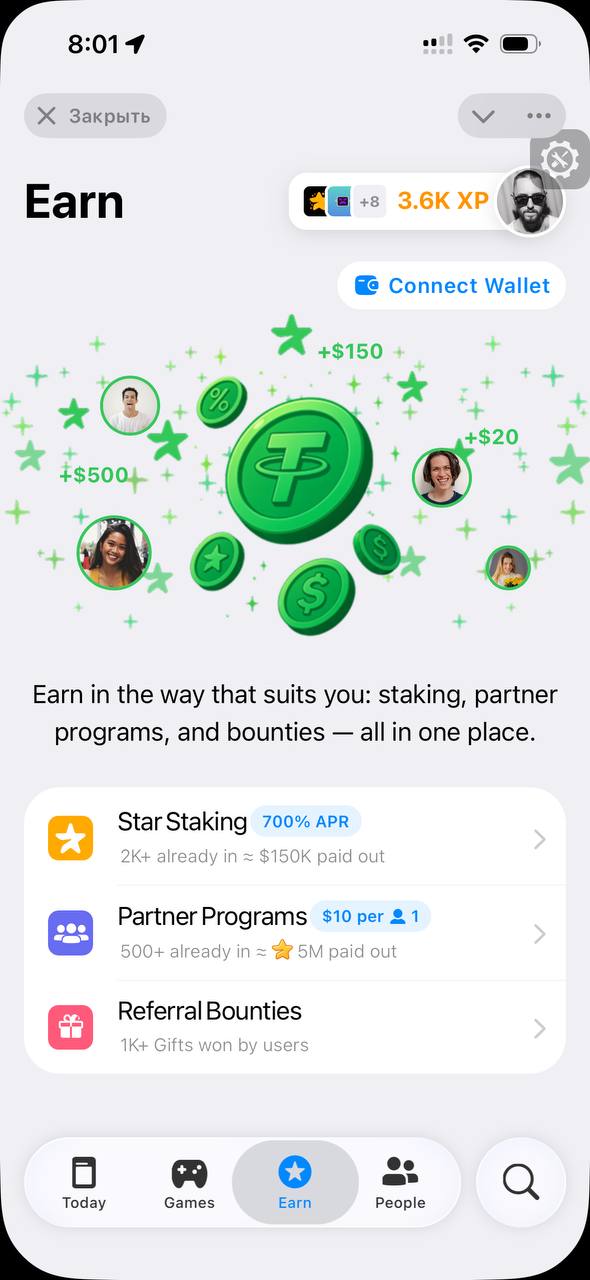

③ Earn, gamified user economy

Star Staking · Partner Programs · Referral Bounties. Regular users earn by helping apps grow. 888K Stars distributed. 700% APR on staking. Aligns user incentives with creator success.

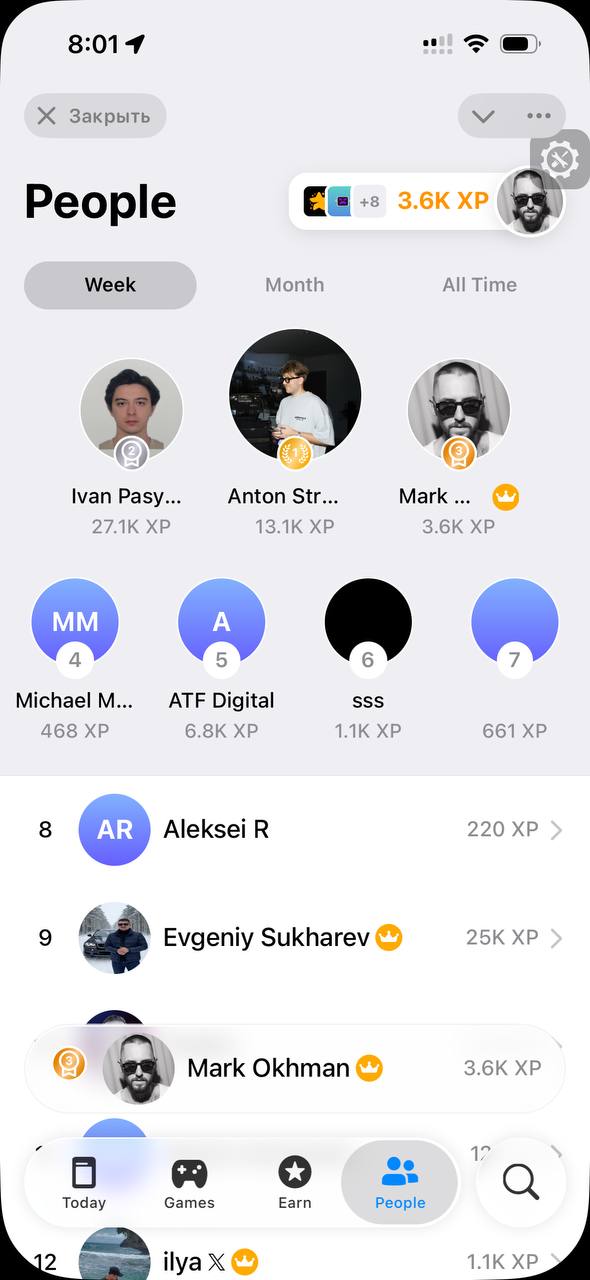

④ Social engagement, discovery follows people

People leaderboards (Week / Month / All Time), XP, influencer profiles showing «what apps am I driving». 490K influencer accounts indexed; 73 verified to date. Each install travels with the user's social context.

«Apple App Store has SEO. We have SEO + Product Hunt + Earn + Influencer-graph, all in one consumer surface.»

UGC means tens of thousands of niches.

Not 200 apps competing for «manicure booking». 20,000, each one personal, regional, niche. That's UGC at the app level.

Native app stores reward consolidation. One «manicure booking» app wins; the other 19,999 die.

UGC platforms reward diversity. YouTube doesn't have one cooking video, it has millions, each personal to its creator. Instagram doesn't have one travel-photographer, it has billions, each with their own aesthetic and tribe.

UGC apps follow the same shape. One manicurist makes the booking app she actually wants to use. She charges her clients $5/mo. She forwards her audience to her favorite product-review app for kickbacks. Her audience is small (100-1,000). She's profitable.

What this implies for our store

Apps Store is not a top-50 ranked list. It's a long-tail catalog of micro-niches. 8K+ apps today on Telegram alone. 100K+ by end of 2027. Each one's audience is small but committed.

«One coffee shop. One booking app for that shop. One product page that ranks for that neighborhood. The atomic unit of UGC apps is the niche, not the category.»

One creator. N apps.

Cross-monetized.

AI coding isn't about replacing developers. It's about letting any creator ship the portfolio of products they always had ideas for.

«I have an idea.»

→ Find engineer → find designer → raise pre-seed → ship MVP → find marketer → realize MVP doesn't work → repeat for 18 months → maybe land. 1-2 apps × 10 years.

«I have 5 ideas.»

→ Ship all 5 in a month. Three die fast. Two grow. Cross-monetize: audience from app A → push offer to install app B → split revenue. 10+ apps × portfolio × cross-traffic.

The old model: one founder → one app → one company. The new model: one creator → portfolio of apps → cross-audience routing. Each app feeds the others. Each new app costs days, not months.

The reframe (vs. typical AI-coding pitch)

Most AI-coding narratives are about cost reduction («developers are cheaper now»). Ours is about self-realization at scale: people with energy, social capital, creativity, who previously hit walls of money/skill/time, can now realize their portfolio of ideas in months.

The bottleneck shifted from «can you ship?» to «do you have audience and ideas?». Both are abundant in creators-with-energy. Engineering was the bottleneck. @appssPro removes engineering as the bottleneck for messenger-app surfaces specifically.

What this implies for @appssPro pricing

Per-app pricing is the right shape. One creator buys 5-10 subscriptions over time, not one. Per-team pricing too as their portfolio grows. ARPU scales without us doing anything.

«AI didn't kill engineers. It unlocked the portfolio creator. We're the OS for that creator.»

An app built in Apps Pro deploys simultaneously into every messenger surface. Platform-specific UI shells are templated; everything underneath is universal.

Universal core (owned by @appssPro runtime)

- Agent identity + harness, system prompt, knowledge base, tool calls

- User state + CRM, single profile across surfaces

- Push notifications, routed through each platform's native channel

- Conversion / purchase logic, Stars · Visa · platform pay

- Cross-platform learning loop, agent improves from every surface

- Discovery + monetization rails, sit above the surfaces

Per-surface UI shells (templated · auto-generated)

- Telegram → full Mini App (webview); WhatsApp → Flow canvas + interactive cards; TikTok → Mini Game / Mini App as SDK opens.

- Messenger / Instagram → DM conversational + Meta canvas; WeChat / LINE / Kakao / Zalo → native mini-program formats; Web fallback → standalone outside messenger.

«React Native = write once, render iOS + Android, UI only. @appssPro = write once, ship a rich agentic experience across every messenger + state + push + CRM + payments + discovery.»

Why platforms can't reproduce this

Meta family is closed to TG / TikTok / WeChat (competitors). TikTok is closed to Meta. Cross-messenger learning is structurally only available to an independent OS, by definition not built by any single platform.

Product lives where you promote it.

Old funnel: 7 hops · 12 months build · 90%+ drop-off. New funnel: 1 hop · days to build · same network for product and promo.

- Build (IDE · codex)12 mo

- App Store / Play review1-4 wk

- Ads cabinet (Meta · TT · G)$$

- Web / IG landing tapUTM

- Download · install−60%

- Onboarding · first action−50%

- Retention D7−80%

- Vibe-coded builddays

- Deploys natively in TG · WA · TikTok1 tap

- Creator posts content in the same networkorganic

- User clicks → app opens in chat0 hop

Legacy app distribution is a 7-step chain. Each step drops 30–80% of users. The cumulative drop-off is 99.5%. To get 100 retained users at D7, a creator pays for ~20,000 ad impressions. That math only works for VC-funded studios.

In-network apps remove every cross-platform hop. The product, the promo, and the user all live in the same surface. User saw a Reel → tapped → app opens in IG DM. No App Store. No download. No UTM. No retention battle for an OS app icon.

Four structural advantages

- CPA collapses. No platform-hop drop-offs. Conversion potential 60× the legacy funnel.

- One person = builder + distributor. Old world needed two roles (engineer + marketer); now one creator runs both in one network.

- Virality is built into the product. Content about the app IS the app's promo. Every user becomes an amplifier.

- Apps become cheap to test. Days to build → can test 20 a year. Quantity over quality of bets, the disposable-app economics from slide 03.

«The product, the content, and the audience finally share one address.»

Tie-back to economics: legacy app CPA is $3–15 per install + 95% drop. Telegram-app CPA settled around $0.05–0.50 per activated user. The funnel collapse is what makes UGC-app unit economics viable.

Three streams. One curve.

SaaS floor · Aggregator ceiling · Partner flows, each compounds with the others as more apps and ecosystems plug in.

SaaS floor (Pro subscriptions). Per-app pricing × per-team. We charge per active app. As a creator ships 5 portfolio apps, they hold 5 subscriptions. Team growth adds per-seat charges. This is the protected downside.

Aggregator ceiling. When one app on our stack breaks out (Notspy did 115K users on stack 1.0, next-gen apps could do 1M+ each), the bulk of those users pass through @appss store to discover the app. They become Store MAU. We can sell that Store MAU as targeted traffic into other apps in the catalog. One unicorn funds the rest.

Partner-program commissions. Creator Market, hire-a-blogger marketplace, takes a fee per transaction. Partner programs (creator-to-creator referral), take a fee per attributed conversion. Each compounds with app count + Store MAU.

Structural alignment vs «vendor lock»

We don't own equity in creators' apps. We don't try to. We own the audience aggregation layer underneath them. Creators get the best deal in the market, best tools, best store distribution, best monetization. We get the audience economics underneath. Both win.

«One App's success funds 100 others. The aggregator economics flip Telegram-app risk from binary to portfolio.»

Telegram first.

Then everywhere.

We're strongest where the substrate has the most ready economy. Then we port the OS, one ecosystem at a time.

TelegramTarget 18 mo · 25K apps · 5K paying Pro · 50M+ store MAU

Reddit AppsWhatsApp AppsTikTok Minis

App Store + PlayWeChat

LINE

Discord

KakaoTalk

Zalo

App Store + PlayWeChat

LINE

Discord

KakaoTalk

Zalo

Telegram first because (a) substrate is most ready, Stars, init_data, channels, bot rails all live; (b) we have 1.5y of production data; (c) Pavel Durov's TON push amplifies our distribution.

Apple + Google next. Native side bridges via Apps store (we cross-list mini-apps and native apps in the same surface). With Apple's Mini Apps Partner Program (Nov 2025, 15% fee), there's now a formal incentive structure for hybrid creators.

TikTok Minis in the same wave because it's the fastest-rolling-out new surface globally (10 regions live, expanding aggressively). Capturing it early matters.

Later wave, WeChat, LINE, KakaoTalk, Zalo, Discord, WhatsApp, each ecosystem we port to is roughly equivalent infrastructure work since the OS shape is the same; only the substrate primitives differ.

«The OS shape ports. The substrate primitives change. The unit economics improve with each ecosystem we cover.»

From Telegram only

to $100M+ ARR by '27.

Three streams × ecosystems closing in sequence. Lovable hit $400M ARR in 12 months, we go for half.

Telegram only Q1 '27

+Reddit Q2 '27

+WhatsApp + TikTok Q4 '27

+Native bridge

The curve isn't a forecast, it's a layering. Each revenue stream from slide 18 compounds with each ecosystem from slide 19. Telegram alone gets us to the ~$5M MRR by Dec 2026 anchor: 5K paying Pro creators × ~$50/mo average + early Aggregator commerce + Partner-flow fees from Telegram + Stars commissions.

Why $100M+ ARR in 2027 is conservative, not aggressive

Lovable hit $400M ARR in 12 months, mostly on a single web surface. We open four additional ecosystems through 2027 (Reddit + WhatsApp + TikTok + native bridge) on top of a Telegram base that already has 1.5y of production data. If each new ecosystem hits even 20–30% of Telegram's ramp curve in year one, the floor is $100M. Hitting Lovable's full curve on the messenger surface would put us at $200M+.

What each stream contributes (rough split at end-of-2027)

- SaaS floor, ~30%. Pro subscriptions × per-team scaling × per-app multiplier. Most resilient, predictable.

- Aggregator ceiling, ~50%. Once portfolio apps cross the 1M-MAU mark each, the @appss store traffic becomes the dominant revenue line. One breakout in any ecosystem moves this number.

- Partner flows, ~20%. Creator Market fees + per-ecosystem partner programs + referral take. Grows in lock-step with the catalog.

«$5M MRR by December funds the SF runway. $100M ARR next year funds the Snapchat-acquirer pitch.»

The shape of the curve matters more than the absolute numbers, every figure on this slide is derived from existing Telegram unit-economics × ecosystem-launch schedule, not from cold-projection.

The math underneath is simple. The in-house content engine generates ~10M monthly views with a ~1–1.5% conversion rate to paid. That conversion already pays our current burn (Loom-funded plus self-generated). We're not asking for money to figure out marketing, we're asking for money to amplify what's already a closed loop.

What «×100» actually means

Today the bottleneck isn't a missing channel. It's our own production capacity. Five creators run the content engine. With ten, output approximately doubles. With twenty plus a paid-traffic layer plus the SEO/AIO indexing flywheel, the same 1–1.5% conversion lands against a 100× larger top-of-funnel. Same proven mechanics, multiplied.

Why partnerships are in the mix

Banks serving SMB segments in target markets have an unsolved problem: their customers need to start earning online, and most SMB tooling is too generic. @appssPro + the @appss store let any SMB ship a Telegram / WhatsApp / TikTok mini-app in days and start monetising the same week. Banks become our distribution layer; we become their SMB-success layer. Neither side has to build the other side.

«We're not raising to discover a growth channel. We're raising to multiply the ones we already proved.»

The team behind

the OS.

Mark Okhman, CEO + founder. Operator-founder, not technical-founder. Multi-year inside the Telegram ecosystem, shipped portfolio apps on top of the substrate (Notspy 115K users live). Owns positioning, fundraising, partnerships, product narrative.

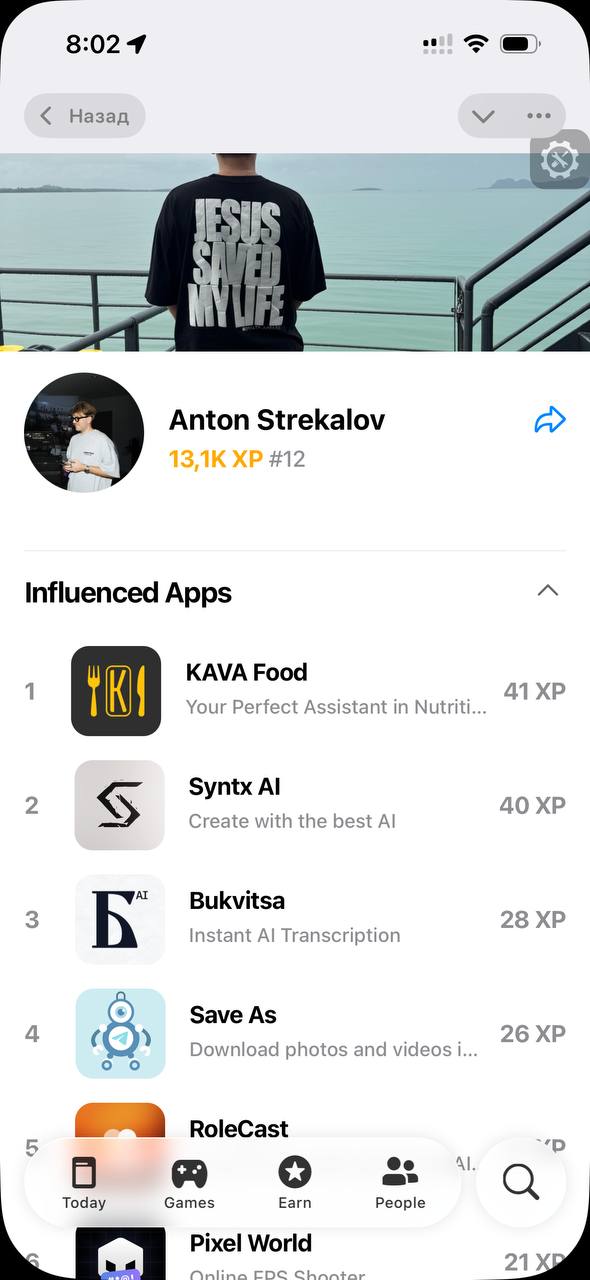

Anton Strekalov, CMO. The marketing engine. Generated the inbound that drove early @appssPro signups (tens of millions of views across IG / TG / YT). Owns the creator-acquisition pipeline + Anton's network of Telegram operators.

Maksim Zhers, CTO. Senior engineer with deep Telegram Mini Apps experience. Owns architecture: builder, hosting, push, store, scoring. The backend that survives 1M+ push deliveries and 49K reviews.

Why this team

You need (a) an operator-founder who eats own stack, (b) a marketer who can recruit creators by their language, (c) an engineer who's already shipped at this substrate's depth. Together = an extremely tight execution machine for the Telegram + messenger-ecosystem play. Each role is irreplaceable.

«Founder + driver + builder. Backed by an investor (Loom) who's been on this thesis since Day 1.»

Current revenue state: @appssPro generating live subscription revenue (per-app + per-team). One portfolio app (Notspy, 115K users) running profitably and self-sustaining. We're not raising to survive, we're raising to accelerate cross-ecosystem expansion.

What $950K buys

- $500K · Telegram growth. Onboard 250M next-gen Telegram users to @appss store + @appssPro. Driven by Anton's marketing engine, supported by store DAU activation.

- $200K · Native Builder. Engineer the iOS/Android port, bridges native + mini-app. Apple Mini Apps Partner Program eligibility baked in. Removes the «we only do Telegram» objection.

- $250K · TikTok expansion. Hire TikTok-oriented onboarding team. TikTok-creator pipeline + TikTok Minis port. First non-Telegram vertical at meaningful scale.

What this round gets you (investor)

Equity in the company that owns the OS layer underneath the messenger-mini-app economy, currently a $-tens-of-billions category opening up in real-time across 11+ platforms. Pricing TBD with lead investor; SAFE-flex available.

«We're not asking you to bet that messengers will become superapps. They already are. We're asking you to bet that we'll be the OS underneath that economy.»